The Wrong Economics Has Been Running Your Business.

Hunter Hastings & Mark Packard · from Venture Mode, releasing May 5, 2026

What passes for economic thinking in most firms isn’t economics at all. It’s central planning — and it’s costing you more than you know.

Capitalism Works. But Not the Way Most Firms Practice It.

The track record of capitalism is extraordinary. Over the past two centuries, it has produced increases in per capita income, life expectancy, material comfort, technological capability, and human freedom that have no parallel in recorded history. Billions of people have been lifted from poverty. Diseases that killed entire generations have been eradicated. The average person today lives a life that the wealthiest monarch of two hundred years ago could not have imagined.

The Value Creators is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

This achievement rests on a specific institutional foundation: the firm. The firm assembles capital, deploys it in markets, creates value for customers, and earns a return that signals where more capital should flow. The firm is the engine of the capitalist system — the mechanism through which individual initiative, entrepreneurial insight, and customer need find each other and produce something new.

And yet, somewhere along the route of this remarkable journey, an error crept in. An error about what firms are, how they work, and what economics actually says about them. That error has been running most businesses for over a century. It is called central planning — and it has been presented, with remarkable confidence, as sound economic thinking.

It is not. And understanding why it isn’t is the key to understanding what Venture Mode is and why it works.

The economic principles that built capitalism have been quietly replaced, inside most firms, by the principles that capitalism was built to defeat.

How Central Planning Captured the Firm

Central planning is the idea that economic outcomes can be improved by designing and managing them from the top down — by setting targets, allocating resources according to plan, and controlling behavior through rules, metrics, and hierarchy. In the twentieth century, this idea was tested at the scale of entire national economies, with results that are now part of history.

But central planning didn’t only colonize governments. It colonized firms. It arrived wearing different clothes — strategic planning, budgeting cycles, management by objectives, KPI dashboards, organizational hierarchies — but it carried the same fundamental assumption: that the people at the top of a system have enough knowledge, and enough control over outcomes, to design the behavior of everyone below them toward a predetermined result.

This assumption is the foundation of what we call Administration Mode. The firm is treated as a machine. The job of leadership is to optimize the machine’s outputs. The people inside the machine are variables to be managed, not agents to be unleashed. And the customer — the person whose life the firm is supposed to be improving — becomes a data point in a model rather than a sovereign individual whose choices determine everything.

The machinery for this kind of management was codified in business schools starting with Frederick Winslow Taylor’s scientific management principles in the early twentieth century — the idea that business could be engineered for maximum efficiency through carefully derived scientific principles. It was refined into the MBA curriculum, which today trains hundreds of thousands of managers annually in the tools of prediction, control, and metric compliance. And it has been embedded so deeply in corporate culture that most executives don’t recognize it as an ideology at all. They think it’s just how business works.

Administration mode isn’t neutral management practice. It is central planning applied to the firm — and it carries all of central planning’s fundamental flaws.

What Economics Actually Says

True economics — the economics that explains how value is actually created in the world — starts somewhere very different. It starts with the individual.

Every person seeks to improve their circumstances. This is not a controversial claim; it is the universal axiom from which economics begins. People are not passive recipients of outcomes engineered by planners. They are active agents, constantly scanning their environment for opportunities to move from a less satisfactory state to a more satisfactory one. They have desires, preferences, and purposes that are irreducibly their own — subjective, personal, and not fully knowable by anyone else.

When individuals seek to improve their circumstances, they turn to others who can help them do so. And here is where entrepreneurship enters the picture — not as a personality type or a startup strategy, but as an economic function. The entrepreneur is the person who senses what others need, even before those needs are fully articulated, and who assembles the resources, knowledge, and capability to provide it. The entrepreneur doesn’t wait for a market research report to confirm demand. They imagine a better future state for a specific customer and build a path toward it.

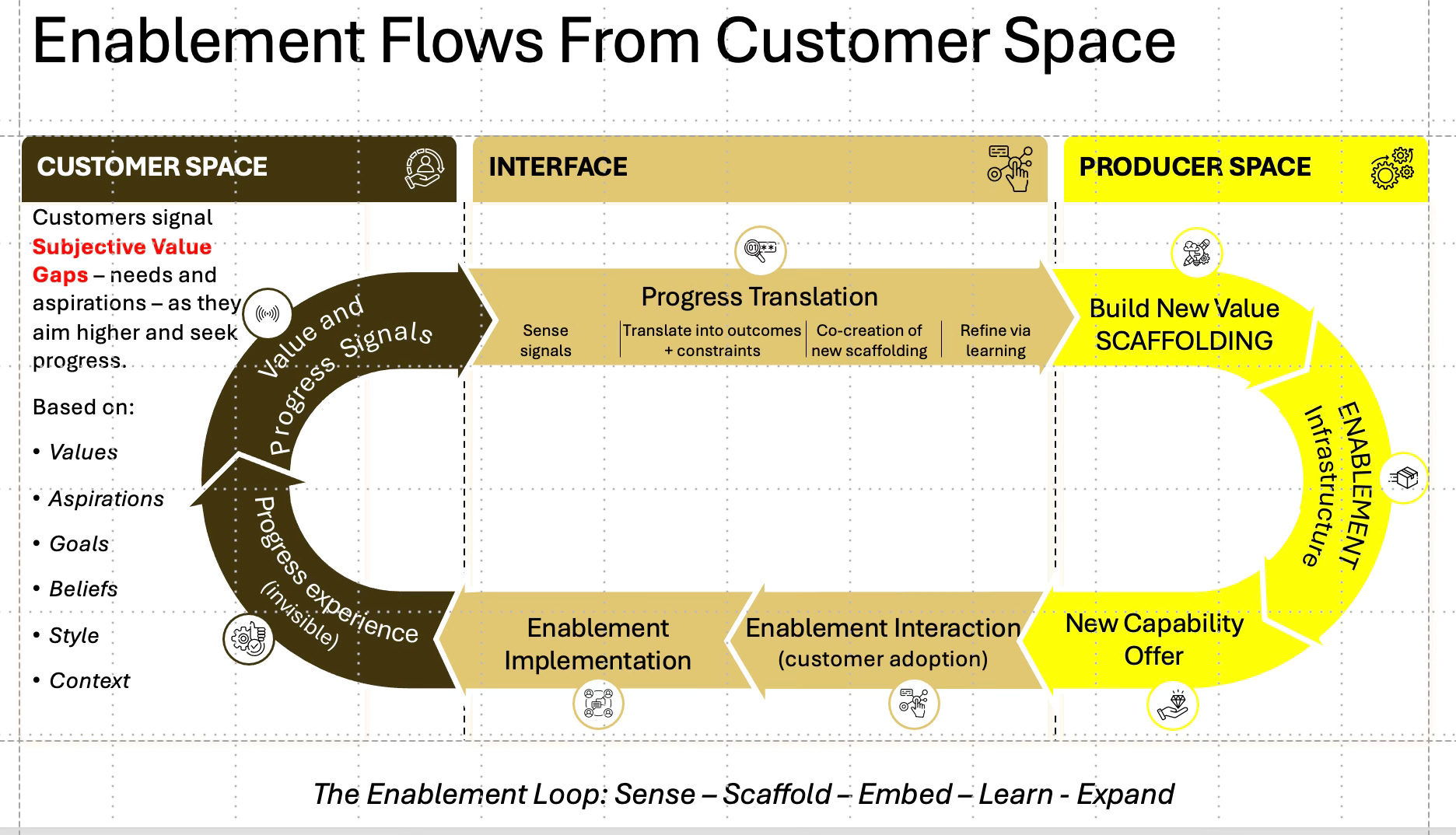

This interaction — between an entrepreneur seeking to provide new value and a customer seeking to experience it — is the atomic unit of economic life. It is where value is created. Not in the boardroom. Not in the planning cycle. Not in the budget process. In the moment when a real person chooses to accept a real offer because it genuinely improves their life.

The customer’s willingness to pay is not merely a revenue event. It is a signal — the clearest signal the economic system produces — that value has been created. And the entrepreneur’s profit is not a extraction from the system but a reward for having served it well: for having sensed a need, borne the uncertainty of attempting to meet it, and succeeded.

Value is not produced inside the firm and delivered outward. It emerges in the customer’s world — in the experience of an improved life — and the firm’s job is to make that experience possible.

The Virtuous Circle — and Why Central Planning Breaks It

When this process works as it should, it is a virtuous circle. Individual entrepreneurs serve individual customers. Customers signal their satisfaction through their choices — choosing again, choosing more, telling others. Those signals guide the entrepreneur toward better offerings and guide capital toward more productive uses. Other entrepreneurs, attracted by the signals, enter adjacent spaces and create new offerings that further expand what is possible for customers. Markets emerge from these countless interactions — not as designed outcomes but as emergent properties of millions of individual exchanges, each one a micro-decision about value.

This is how capitalism produces prosperity. Not through planning. Through the distributed intelligence of people pursuing improvement, guided by the feedback of free exchange.

Central planning breaks this circle at every point. It substitutes the judgment of planners for the judgment of customers. It replaces the signal of voluntary exchange with the noise of internal metrics. It directs capital according to predetermined allocations rather than toward its highest and best use as revealed by actual market feedback. And it suppresses the entrepreneurial sensing function — the ability to discover what customers need before they can fully articulate it — by replacing it with process compliance and approval hierarchies.

The energy of an economic system originates at the interface between entrepreneur and customer — in the trillion individual interactions where need meets capability, where imagination meets desire, where value is discovered rather than planned. Central planning at the firm level doesn’t tap that energy. It blocks it. It installs layers of management, compliance requirements, and metric systems between the entrepreneur and the customer, damping the signal at every layer until very little of it reaches the people who could act on it.

The energy of economic growth originates at the interface between entrepreneurs and customers. Central planning — whether in governments or firms — installs barriers between them and calls it management.

Entrepreneurial Economics at Work

This is not a theoretical argument. It is visible in every high-performing organization that has broken free from administrative control.

The firms that have created the most economic value in the past twenty years share a common characteristic: they operate as networks of entrepreneurial interactions rather than as hierarchies of administrative control. Amazon is a platform through which millions of entrepreneurs interact with millions of customers, with capital flowing continuously toward the interactions that create the most value. Apple under Steve Jobs was organized around the sensing function — Jobs’s extraordinary capacity to imagine what customers would want before they knew they wanted it, and to build organizations capable of delivering it. Airbnb’s recovery under Brian Chesky began when he abandoned conventional administrative wisdom and returned to the founding insight: that the firm exists to serve the customer, and that the people closest to the customer have more relevant knowledge than any planning cycle can capture.

These are not anomalies. They are demonstrations of entrepreneurial economics operating at scale. They show what happens when firms are organized around the atomic unit of value creation — the entrepreneur-customer interaction — rather than around the administrative machinery that sits between that interaction and the leadership of the firm.

The Silicon Valley ecosystem represents the most visible contemporary expression of entrepreneurial economics. It is not primarily a geography or a culture. It is a structure: a dense network of entrepreneurs and customers in continuous interaction, with capital flowing rapidly toward the interactions producing the most value, and with minimal administrative friction between the sensing of customer need and the delivery of new value. Its outperformance of traditional corporate models is not accidental. It is the predictable result of entrepreneurial economics operating closer to its native logic.

The Institutions That Got Left Behind

The tragedy is that the institutions best positioned to spread entrepreneurial economics — large firms with deep market knowledge, established customer relationships, and access to capital — are also the institutions most thoroughly captured by administrative central planning.

The MBA-trained executive understands budgets, org charts, strategic planning cycles, and performance management systems. These are the tools of central planning applied to the firm. What they do not teach — what business schools have systematically failed to develop — is the entrepreneurial sensing function: the capacity to imagine a better future state for a specific customer, to bear the uncertainty of pursuing it, and to organize resources around discovery rather than execution of a predetermined plan.

Business schools are not a neutral party in this story. They have been the primary mechanism through which central planning assumptions have been transmitted into corporate culture, generation after generation, credential by credential. The MBA curriculum is not the cutting edge of management science. It is the codification of administrative mode — the formalization of central planning principles into a teachable, certifiable, hireable package.

And universities themselves, as we examine in Venture Mode, are among the most perfectly realized examples of administration mode in existence — hierarchical, compliance-driven, metric-obsessed, and deeply resistant to the entrepreneurial disruption that has improved quality and reduced cost in virtually every other sector of the economy.

The institutions most capable of spreading entrepreneurial economics are the ones most deeply captured by its opposite. That is the administration trap — and escaping it requires understanding what trap you are in.

What This Means for Your Organization

If your organization runs on strategic planning cycles, budget approvals, KPI dashboards, and hierarchical decision rights — if the primary language of leadership is hitting targets, managing variances, and ensuring compliance — then it is running on central planning assumptions. It is organized around the prediction and control of outcomes rather than the discovery and creation of value. And it is suppressing, at every level of the hierarchy, the entrepreneurial energy that is the only sustainable source of the growth you are trying to plan into existence.

Venture Mode is the application of entrepreneurial economics to the organization. It means organizing around the atomic unit of value creation — the interaction between an entrepreneurial leader and a sovereign customer — and removing every administrative layer that stands between that interaction and the firm’s resources, decisions, and leadership attention.

It means replacing the central planning of targets, budgets, and compliance systems with the distributed intelligence of people close to customers, empowered to sense needs and experiment toward solutions. It means letting capital follow value creation rather than directing value creation toward where the capital has already been allocated. It means treating uncertainty not as a problem to be managed but as the natural condition of entrepreneurial discovery — and building organizations designed to navigate it rather than pretend it doesn’t exist.

The economics has always been on the side of the entrepreneur. The firm that organizes itself around entrepreneurial economics — that puts the customer at the sovereign center, that trusts its people to discover rather than comply, that treats every customer interaction as a signal to be learned from rather than a transaction to be processed — is not taking a risk. It is aligning itself with how value is actually created in the world.

Everything else is central planning. And central planning, as history has demonstrated at every scale at which it has been attempted, produces the same result: the accumulation of power at the top, the suppression of energy at the edges, and the steady erosion of the very thing it claimed to be optimizing.

Venture Mode is not a management methodology. It is the application of sound economics to the organization — the economics of entrepreneurship, discovery, and customer sovereignty that capitalism was always supposed to embody.

Hunter Hastings and Mark Packard are the authors of Venture Mode: Escape the Administration Trap by Finding and Unleashing Entrepreneurial Leaders, releasing May 5, 2026.

This is one of a series of articles drawing on the book’s core arguments. Learn more at venturemode.biz